KRBL Ltd - The Big Daddy of Indian Basmati rice is back.

I wrote the article in June 2025, unfortunately it was not published.

I’m sharing the same article with minor changes for you. Please read in conjunction with Q1FY26 (June 2025) results, the story gets better.

Special thanks to Hitesh R for bringing this idea to my notice.

KRBL: The Basmati Giant’s Rollercoaster Year – From Slump to Surge

Investing can be as simple – and as complex – as cooking a pot of biryani. You need the right ingredients, timing, and a dash of patience. KRBL Ltd., the company behind the famous India Gate basmati rice brand, is proving the point to its shareholders.

KRBL stock had hit a 52 week low of Rs 253 per share is now trading at Rs 355 per (25th June 2025) share on the back of improving margins and solid year on year growth of 26% in March 2025 quarter.

Challenging first half of FY25

Just a few months ago, KRBL was struggling. In Jun 2024 quarter revenue fell 15% year-on-year to ₹1,199 crore, and net profit plunged 55% (to about ₹86.6 crore). That marked the fourth straight quarterly profit decline.

The reasons weren’t all internal: weak demand and government induced disruptions on rice exports created a perfect storm. As a result exports dropped during the first half of FY25. While basmati rice exports weren’t banned, the government imposed a steep minimum export price (MEP) of $1,250/MT initially, making Indian basmati less competitive globally.

This, combined with payment issues in key markets like Iran and Iraq, led KRBL to voluntarily scale back bulk exports to avoid credit (receivables) risk—resulting in a sharp year-on-year decline in overseas volumes.

Profit margins were squeezed as basmati prices fell even as paddy (raw rice) costs remained high.

A turnaround during Second half FY25

By quarter ending December 2024, KRBL’s sales were bubbling up again with ₹1,682 crore in consolidated revenue, up 17% from the same quarter a year ago.

This resurgence was driven by a strong rebound in exports, which surged by around 27.6% in Q3 (y-o-y) and by 44% in Q4(y-o-y), while domestic sales held roughly flat.

Profitability stabilized too: KRBL earned ₹133 crore net profit in Q3 and ₹154 crore in Q4FY25, roughly the same as the year-ago period (after being significantly lower in the first half).

While on full year basis, FY25 profits are down 21% compared to FY24, the second half of FY25 highlights an improving trend.

In second half of FY25, export revenue grew 44% in Q4. While domestic revenue was flat. Even more heartening, profit margins improved markedly – EBITDA for Q4 came in at ₹223.7 crore (up 25% YoY) with the EBITDA margin expanding to 15.5% from 13.5% a year earlier.

After a year of cost inflation chewing into profits, KRBL finally got relief as input prices stabilised and its premium rice commanded better pricing.

🚦Timely, differentiated insights require a LOT of hard-work. If you like my work, please consider contributing INR 300 or upwards on UPI: rk4g10@okhdfcbank or scan the QR code at the bottom of this article. ☺️

The chart below captures this change in fortunes: after a lukewarm FY24 and early FY25, overall revenue grew 4% in FY25 (with basmati volumes up 5% for the full year).

High margin, low growth equals low valuations

KRBL Ltd enjoys higher margins compared to peers such as LT Foods and Chamanlal Setia Exports. Yet, the valuation (PE – 17, P/B – 1.6x) it gets is significantly lower than these peers.

There could be a couple reasons for this dichotomy :

Slower Growth – Over the last 5 years, KRBL ltd has grown sales at a compounded rate of 4% and profit at -3%. It’s hardly the kind of growth that gets investors excited.

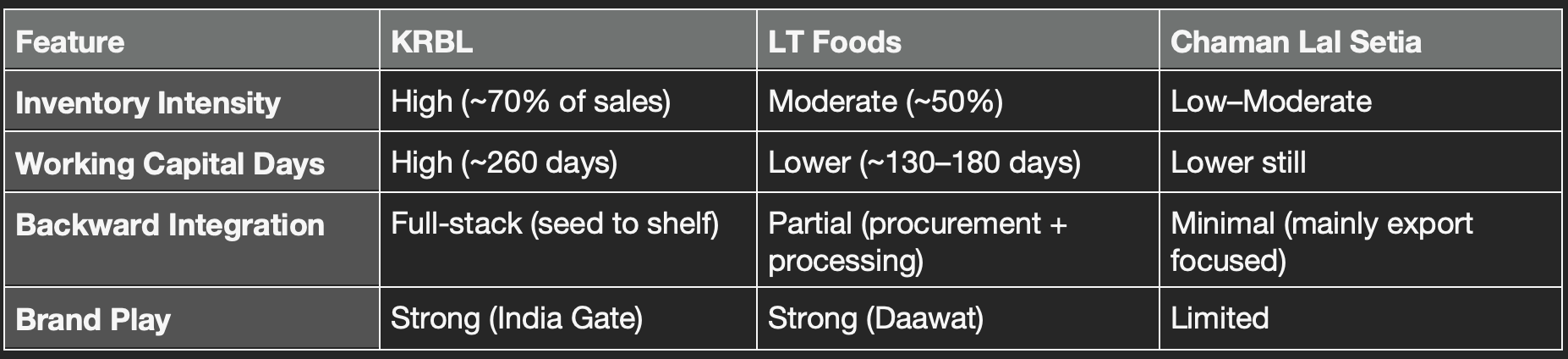

High Inventory Model – Compared to peers such as LT Foods which have exposure to markets such as the US, KRBL has large exposure to Iran & Iraq, countries that have volatile currencies and economies and longer payment cycles.

High backward integration & High working capital – Unlike LT Foods and Chamanlal setia, KRBL ages its basmati rice for a longer duration to enhance quality. Longer ageing increases the quality of the basmati rice.

Additionally, it also has large scale contract farming operations and tends to hold large amount of inventory by virtue of its longer ageing process. Longer ageing of basmati rice increases its quality but also holds back large amount of capital in inventory.

For example, in Q4FY25, it held ₹ 3,600 crore of inventory compared to FY24 which is about 65% of FY25 sales.

For context, LT foods’ inventory is about 50% of sales.

Governance concerns

KRBL has long carried a governance overhang due to its alleged link to the 2018 AgustaWestland VVIP chopper scam. In that case, its Joint Managing Director (JMD) was named in connection with financial transactions tied to middlemen. The matter resurfaced in March 2024, when the Enforcement Directorate (ED) conducted searches and filed a criminal complaint against the company, its Dubai subsidiary (KRBL DMCC), and the JMD under the Prevention of Money Laundering Act.

As per Note 7 in its financials, an independent review found no conclusive financial impact, but the investigation is ongoing, keeping governance risks in investor focus.

For these reasons perhaps KRBL, despite being a market leader has not been able to command valuations as high as its peers.

Peer comparison – Inventory & Working capital

Addressing Growth Concerns

KRBL is transitioning into a multi-brand FMCG play, anchored on the India Gate brand. In FY25. It has gained Market share by 2-3% in Basmati rice across general trade, modern trade and e-commence channels according to Nielsen data highlighted in the company’s Q4FY25 investor presentations.

It has also increased distribution by adding 51,000 outlets in FY25 (now 4.09 lakh. In terms of brand Push the company recently announced Amitabh Bachchan as brand ambassador.

Product Expansion

The company has expanded its ‘Regional Rice’ which is expected to contribute about Rs 250 cr in FY25 (data not confirmed in Q4 presentation). Regional rice refers to non-basmati, locally preferred rice varieties like Sona Masoori, Gobindo Bhog, and Kolam, tailored to regional taste preferences across India.

It introduced India Gate Biryani Masala that already holds 3% market share in Modern trade & Q-commerce channels.

KRBL also has recently introduced Uplife (Edible Oils) and targets ₹70–75 crore in Year 1, ₹300 crore by Year 3.

A chance in product mix should help the company rev up its poor growth metrics.

Exports to support Growth

Not only has the recent trend in exports been strong in Q3 & Q4 but the company is also targeting re-entry into Saudi Arabia with two wholesalers with a target sales of ₹500 crore in FY26.

KRBL’s exports to Saudi Arabia were suspended in early FY24 due to a dispute with its exclusive distributor in the country. The exact reasons were not disclosed in detail, but investor commentary and filings suggest:

KRBL had a long-standing arrangement with a single Saudi wholesaler.

This relationship broke down, possibly due to pricing disagreements, credit/payment issues, or a misalignment in brand positioning.

As a result, KRBL temporarily exited the Saudi market, which is a key basmati-consuming geography and had previously contributed significantly to export revenues.

Progress on Governance Concerns

The ongoing ED investigation relates to KRBL’s JMD and alleged links to the 2018 AgustaWestland scam. As per Note 7 to the FY25 financials, a criminal complaint has been filed against KRBL, its Dubai subsidiary, and the JMD. An independent firm’s review found no conclusive financial impact so far, though the case remains sub judice.

Valuation: A Value Pick or Fairly Priced?

The stock hit 52-week lows around ₹226 last year when earnings were under pressure. At that price, KRBL was trading at roughly 1.0x book value.

Fast forward to today, and optimism has crept back in. KRBL now trades around ₹350–360. That puts its valuation at roughly 17x trailing earnings and about 1.6x book value.

These multiples – a P/E of ~17 and P/B ~1.6 – are hardly exorbitant, especially when compared to peers such as LT Foods and Chamanlal Setia Exports.

As discussed, this could be because KRBL’s long-term growth has been unspectacular. Revenues have grown just ~4–5% annually over the past five years, and Return on capital employed (ROCE) has dropped to a low of ~12% in FY25. Not to mention again, the governance concerns that have been ongoing since 2018 and resurfaced in 2024. Those figures explain why KRBL hasn’t commanded high-flying multiples like some other peers.

The Bottom line is KRBL has shown resilience by bouncing back from a tough year with a strong finish. It’s a solid, if unspectacular, business is trading below its 5 year median P/B value of 1.7x (at 1.6x). For retail investors, that could be an appealing recipe – a market leader with manageable risks and improving growth potential.

Rahul Rao, CFA

🚦Timely, differentiated insights require a LOT of hard-work. If you like my work, please consider contributing INR 300 or upwards on UPI: rk4g10@okhdfcbank or scan the QR code at the bottom of this article. ☺️

DISCLAIMER:

Nice write-up! I had looked at both KRBL and LT Foods in early-2024 and decided to invest in LT Foods, which I still own currently. KRBL also looks interesting, but the legal case and history prevented me from buying. Will look again now

I would still hold my LT Foods over KRBL. Invested in LT at ~100 levels when in my work visit to Saudi; realised that they were all over the shelves even before the KRBL issue with Saudi Importer happened