Micro-finance Turnaround?

Byte #8

Of the 13 listed Microfinance / Small finance banks, 6 have reported quarterly business updates so far.

Bandhan Bank

ESAF SFB

Equitas SFB

Ujjivan SFB (Disclosure: Invested)

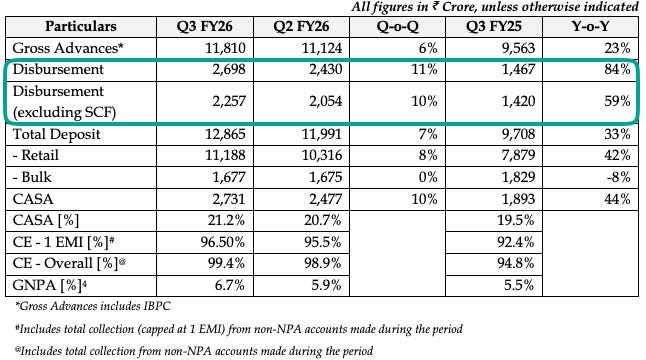

Suryoday SFB (Disclosure: Invested)

Capital SFB (Disclosure: Invested)

Here’s a compilation of key metrics that matter for this group and a feeler on whether the turnaround is indeed happening or not.

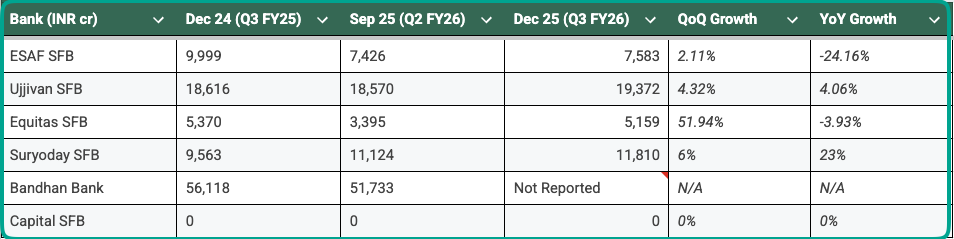

1. Gross Advances - MFI Loans.

The table below shows only MFI loans outstanding as on December 2025 quarter.

You’ll notice that Equitas SFB QoQ jump is significant but setting the context is essential. While QoQ growth is impressive, on a YoY basis there has been a marginal degrowth. Secondly, Equitas SFB was one of the first SFBs (Capital SFB not in MFI loans entirely) to wash its hands off the MFI segment.

This was seen as a positive when sh*t was hitting the proverbial fan but turns out without MFI segment - Risky but high yielding & profitable during good times - Equitas was going to have a hard time hitting an ROE of 13-15%.

Its too soon to say that they’ve done a U-turn on their “move away from MFI” strategy - something all SFBs have been attempting at their own pace. The likely reason for a rapid QoQ increase is opportunity presented itself to grow MFI loans & Equitas took it.

Since Gross loans are INR 43,269 cr, INR 5159 cr of MFI loans is about 12% of Total Gross loans outstanding.

Then, there’s Ujjivan. It’s numbers on the surface looks flattish.

However, a breakdown shows that Ujjivan too (including Arman Financial) is focusing Individual MFI loans vs Group loans.

Finally, Suryoday SFB - the dark horse. Both the QoQ & YoY are impressive.

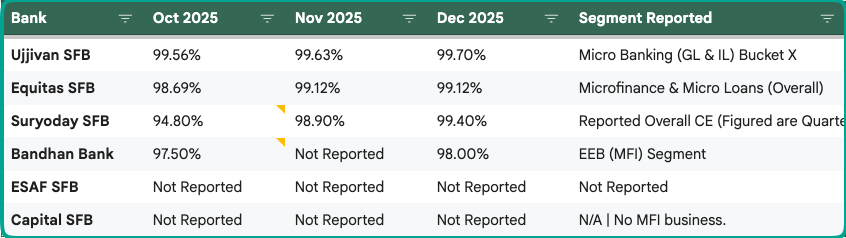

2. Collection Efficiency

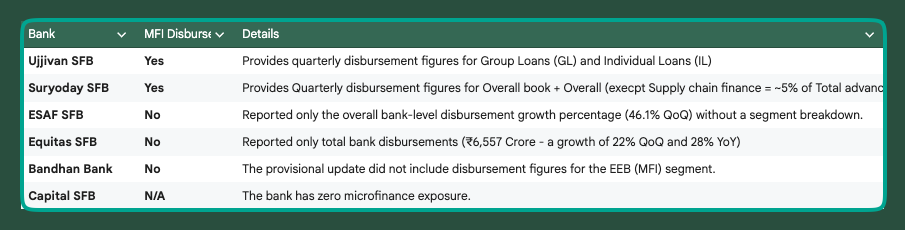

3. Disbursement growth

The data has not been uniformly reported across all SFBs in this subset. Barring Ujjivan, which has the comprehensive reporting structure & suryoday which reports disbursement figures on a quarterly basis BUT not as detailed as Ujjivan’s, no other SFB has reported granular disbursement numbers.

This is either a case of poor communication or unwillingness to share information openly or both. When you don’t have much to brag, you probably don’t.

Suryoday SFB’s disbursement growth is really encouraging.

4. Turnaround or not

In a post on X, I had shared that a turnaround is not uniform. The better players, especially as far as financials are concerned are likely to turnaround faster than the pack.

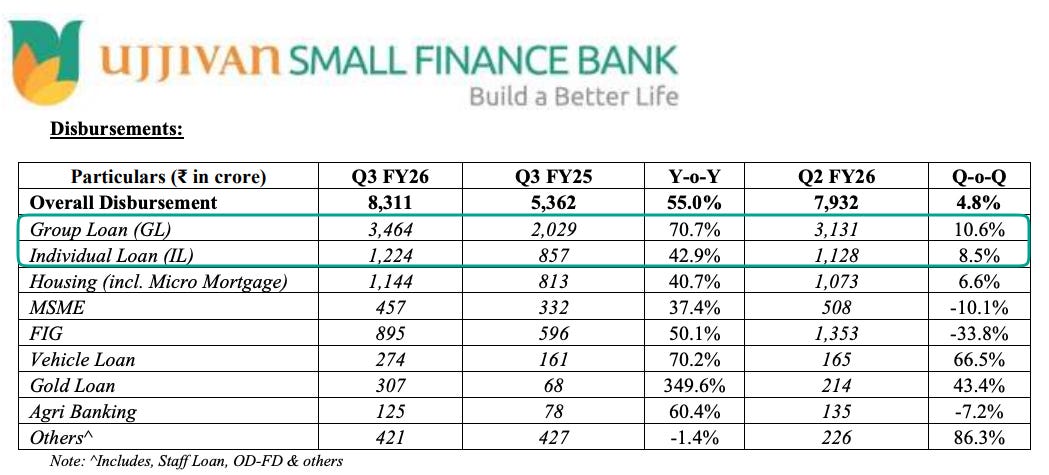

Ujjivan SFB is one of those players. However, for Housing (incl. micro-mortgage) is now 25% of the book & growing at 49.6% YoY. This pace makes me a little uncomfortable.

“secured,” affordable housing collateral is much lower quality than we believe. Such loans are also expensive to recover given the outstanding is usually a few lakhs unlike prime housing where it pays to go after recovery where your outstanding in tens of lacs or even crores. Anyway, high growth requires closer tracking.

Net net: A stellar comeback story !

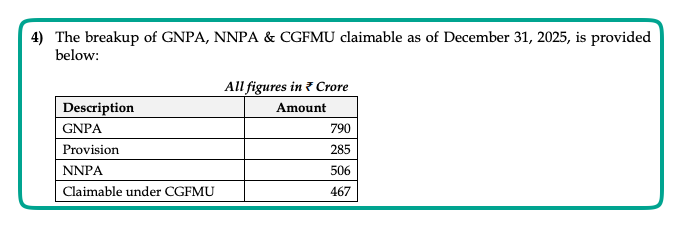

Suryoday SFB is also showing strong signs of revival. Of the INR 506 cr of NNPA, INR 467 is claimable under CGFMU. What’s comforting is that the SFB has already received CGFMU dues of INR 314 cr in September 2025, removing a massive overhang.

FYI, we’re starting a new batch of our DIY Investing Framework from 11th January 2025. This LIVE ONLINE program is curated to help Individual retail investors apply some key frameworks that work in the markets.

AND we have a New Year Offer - A massive discount. You can scan the QR code below or click here to signup !

Regards

Rahul Rao, CFA

no suryoday small finance bank in the post?