Hidden Aluminium stock

Akkineni Nagheswar Rao (ANR) was born to a farming family in Ramapuram Village, Andhra Pradesh in 1923.

His formal education was limited to primary schooling due to his parents' poor economic condition.

He began working in Theatre at the age of 10. But the turning point of his career came when a prominent film producer discovered him at Vijayawada railway station. He helped ANR debut in Dharampatni (1941).

The rest - is History, as they say.

He starred in over 255 films, spanning the Telugu, Tamil and Hindi languages & was awarded all three Padma Awards - Padma Shri, bhushan, vibhushan in 1968, 1988 & 2011 respectively.

Basically, a legend of the Telegu film industry.

ANR married Annapurana & together they had 5 children - Sathyavathi, Venkat, Susheeila, Saroja and Nagarjuna Akkineni.

In the mid-970’s, ANR opened a studio - Annapurna Studios, whose operations were handled by Venkat, by then an MBA Grad from University of Wisconsin, USA.

If you’re wondering why this matters & what’s it gotta do with our “niche aluminium player”?

Wait.

Origin story

Our “Niche Aluminium player” was incorporated in in 1984 by V S Prasad & K Ramachandra Reddy, possibly in anticipation of certain Industry deregulation.

However, operations did NOT commence until 10 years later in 1995.

Fun fact:

K Ramachandra Reddy is also a University of Wisconsin graduate (like Venkat) & the son of K.V. Reddy (Kadiri Venkata Reddy), who is arguably one of the most respected directors in the history of Telugu cinema.

K Ramachandra Reddy is also the founder of Moschip Semiconductor Ltd (MCAP: INR 3900 cr)

Remember that during the 70’s & 80’ Government of India set interest rates & controlled prices of key commodities.

It was a total sh*t show.

The Aluminium control order of 1970 mandated 50% of the Aluminium metal sales to state electricity boards (for Rural Electrification) at Govt controlled prices. Not surprisingly, these SEB’s were broke. The GOI also restricted/controlled technology tie-ups with global aluminium leaders.

In 1989, Cement & Aluminium sectors are de-regulated.

In 1991, Aluminium sector was “de-licensed”.

This made foreign collaborations and import of capital goods possible, which previously attracted import duties as high as 100% or more.

German cars still do. The “Mother of all deals” is set to change all that.

Could it be a co-incidence that Venkat Akkineni (VA), ANR’s son, an MBA from the University of Wisconsin (1970), decided to come onboard at exactly the time when Aluminium was de-regulated in 1991?

I don’t know. Good timing? It definitely was.

VA was 37 years young by 1991 when he became involved with Alufluoride Ltd. By then he had been managing Annapurna studios since the mid-1970’s. By some accounts (ISB Case study) - not very successfully.

The studio was struggling till his younger brother Nagarjuna Akkineni became an actor & started shaping the studios’ activities in his vision (1999).

VA possibly got involved because because V S Prasad - founder & company’s MD at the time, suddenly passed away. The other co-founder - K Ramchandra Reddy (Founder - Moschip technologies Ltd) probably found managing a chemical co’ too boring?

Either ways, this was a chance for VA to get involved with something NEW.

After all it was 1991: Economic liberalisation, de-licensing, opening up the economy, a hot stock market - why wouldn’t a young entrepreneur take a chance?

The early days (1991 onwards)

Between 1991 & 1994, Mr. Venkat Akkineni oversaw the technical tie-up with Alusuisse (Swiss Aluminium Ltd.) to validate the “wet process” technology, financing of the project, getting the raw material tie-up (Hydrofluorosilic Acid) from Coromandel International Ltd (Adjoining plant in Vizag).

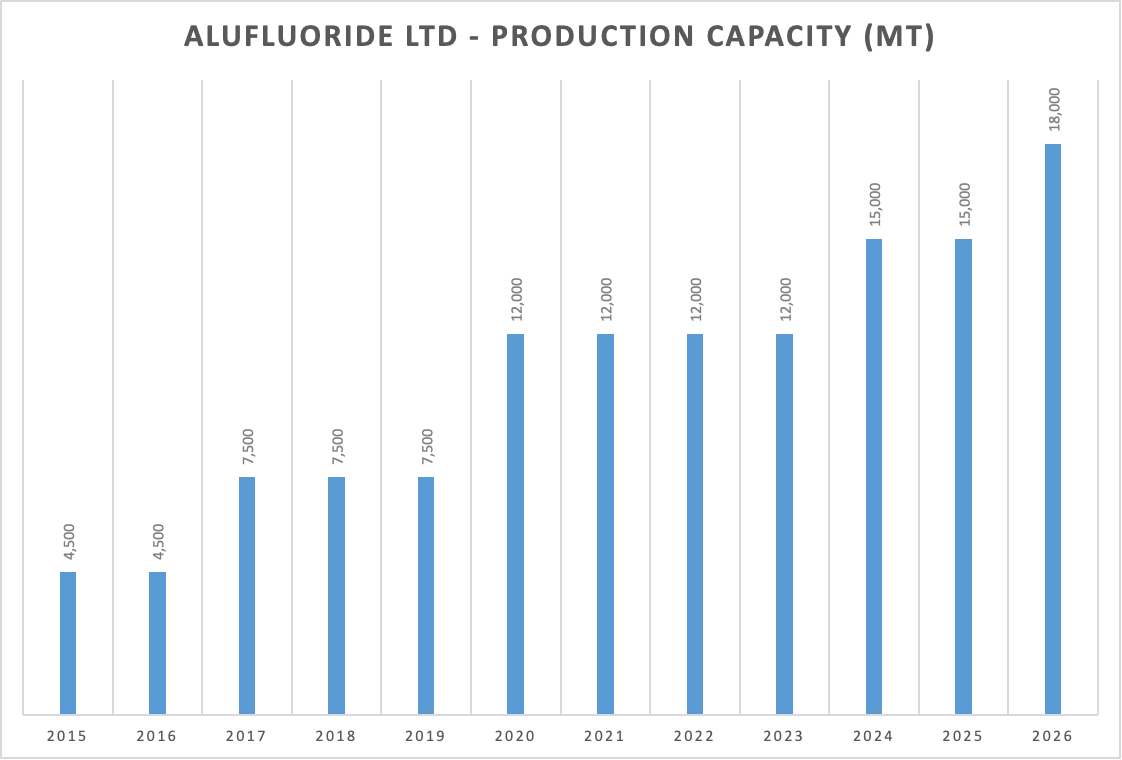

The company went public in July 1994 to finance this vision & listed on the Bombay with an oversubscription of 25X. It commenced production in 1995.

From 1995 to 2011 - Installed capacity increased from 3,000 MTPA to just 6,000 MTPA.

Then in 2017, capacity increased to 7,500 MTPA & all the way to 18,000 tonnes per annum (TPA) in May 2025.

What happened in 2017?

Venkat’s son - Aditya Akkineni steps into the business. The fact that in the nearly 20 odd years the companies capacities barely doubled despite Aluminium smelting capacity having grown leaps and bounds, our niche aluminium company failed to grow.

Management matters. More on this later.

Business

The co’ sells Aluminium Fluoride aka Alufluoride (ALF).

1. What is Alufluoride?

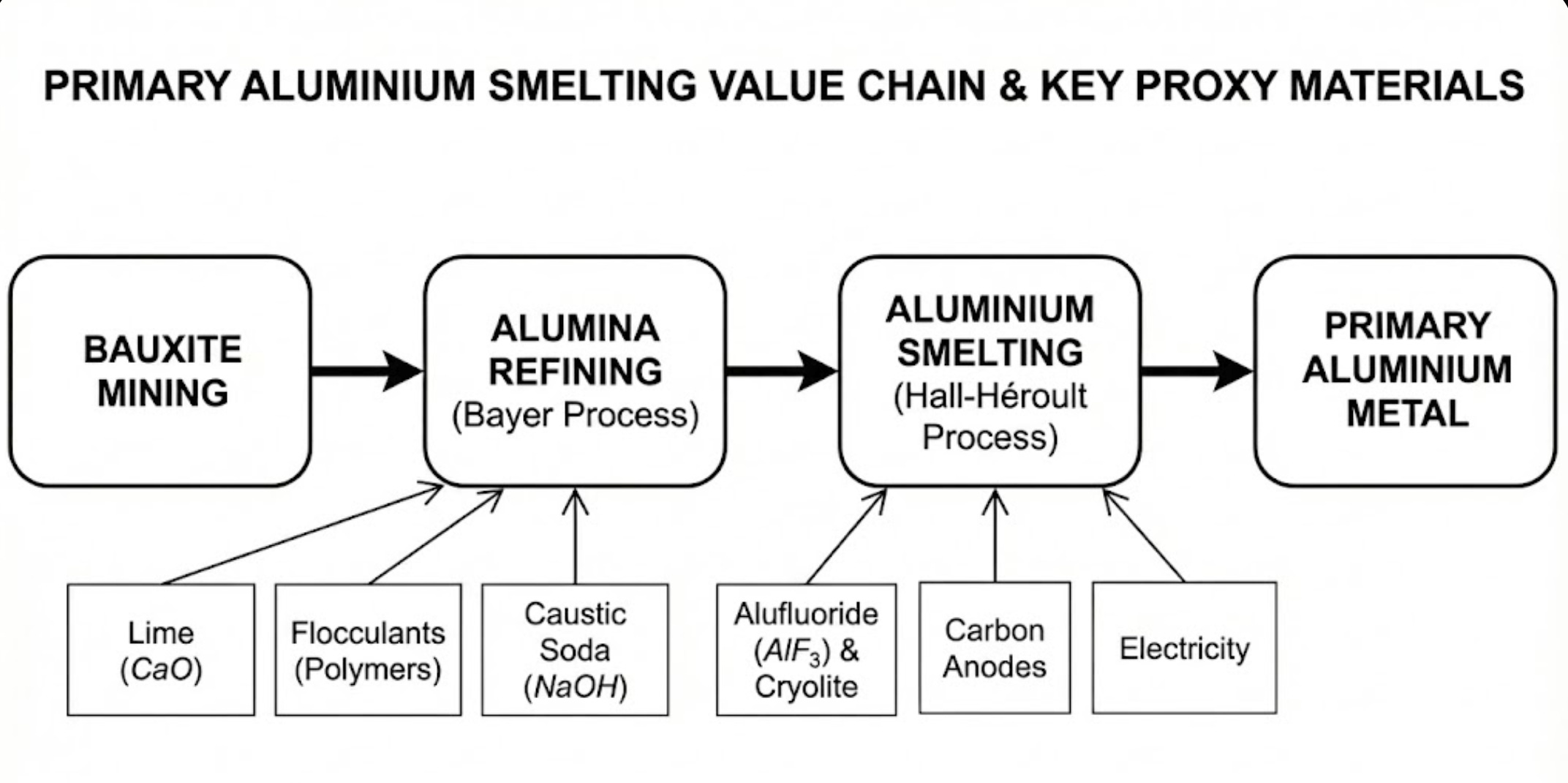

Alufluoride (ALF) plays a CRITICAL role in the Hall-Heroult process.

We explained the Auminium Value chain & the Hall-Heroult process in our recent deep-dive on the Industry.

In short, Alumina (powder) is mixed in cryolite (non-reactive liquid) & Alufluoride (powder). A “pot” filled with this mixture is subjected to 300 KA to 600 KA current.

This helps separate Aluminium atoms from Oxygen.

Let’s go deeper.

Cryolite (molten bath - Non-reactive) lowers the melting point of Alumina to ~1010°C

Aluminium fluoride FURTHER lowers it to 950°C - 960°C.

This lowering of 50°C - 60°C might seem like whatever.

Toh kya.

It singlehandedly makes the process of Aluminium smelting economically viable.

Let’s go another step deeper…

Alufluoride’s key role is to improve Current Efficiency in three simple ways:

It Acts as a Coolant: It lowers the melting point of the smelting bath from over ~1000°C to around ~960°C . This cooler temperature prevents the aluminium you just made from vaporising and being lost.

It Saves Electricity: By improving the conductivity of the molten bath, it allows electricity to flow more easily, meaning less energy is wasted as heat and more is used to make metal.

It Separates the Metal: It helps the pure aluminium sink cleanly to the bottom of the pot, keeping it safe from reacting with gases and turning back into waste.

POINT IS: IT IS SUPER F*CKNG CRITICAL !

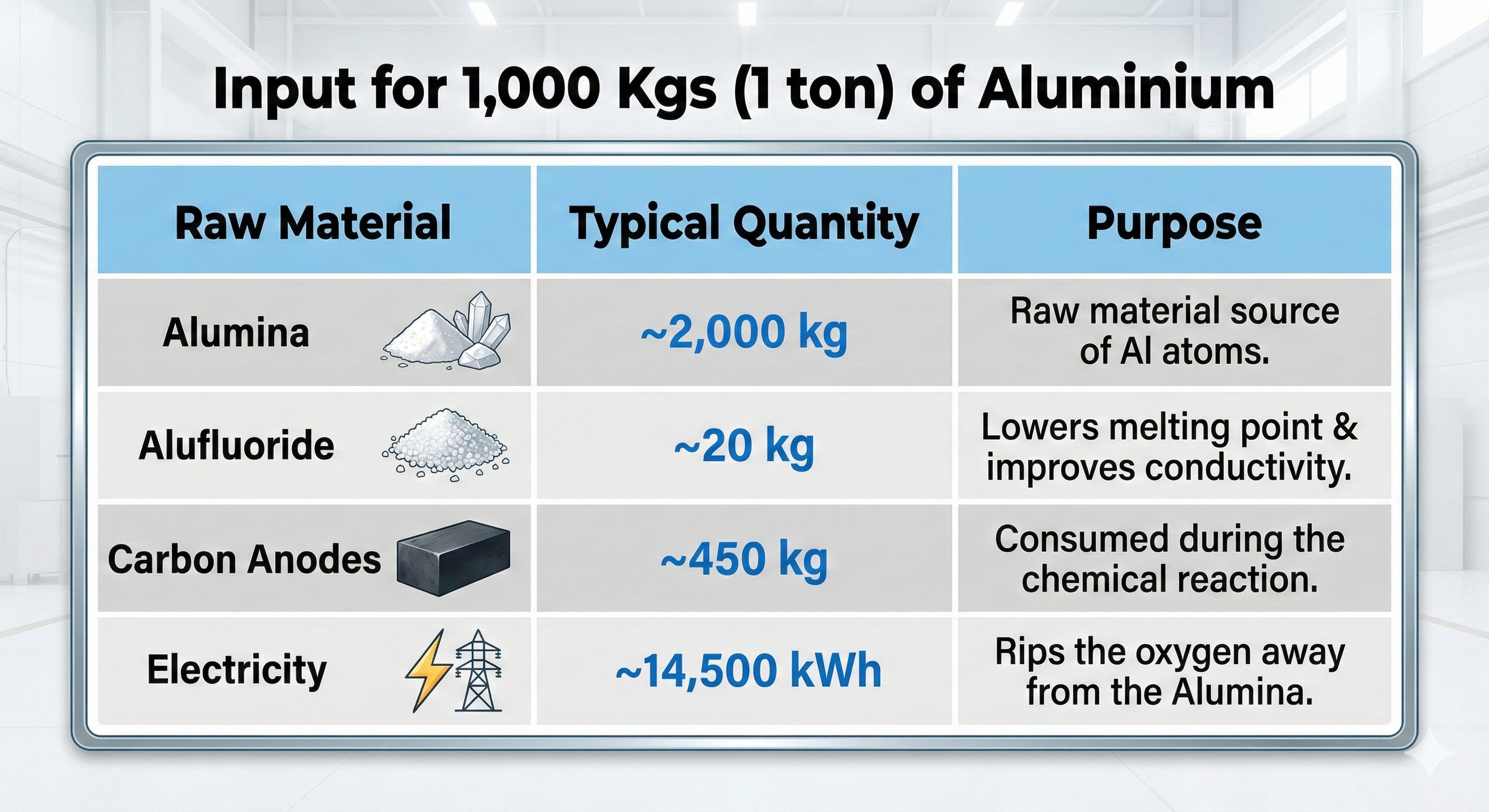

AND because only ~20 Kgs of Alufluoride is required for EVERY 1 ton of Aluminium…

Alufluoride, my friends, is NOT ONLY…

A. SUPER CRITICAL !

BUT ALSO

B. IT MAKES UP FOR A FRACTION OF THE OVERALL COST STRUCTURE.

Need I say more?

2. How it’s made?

First, let’s breakdown WTF ALF is:

Bonds made up of

Aluminium.

Fluorine.

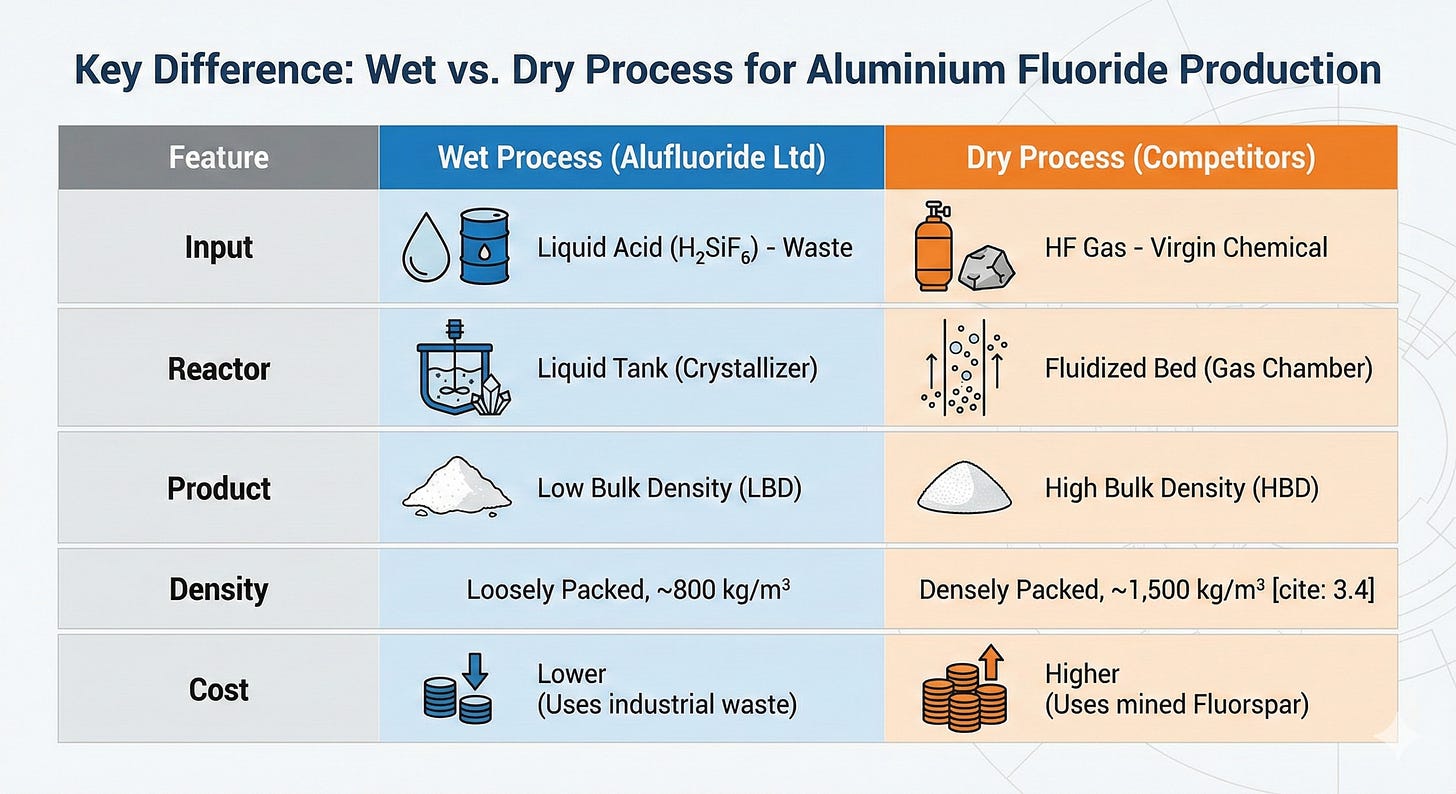

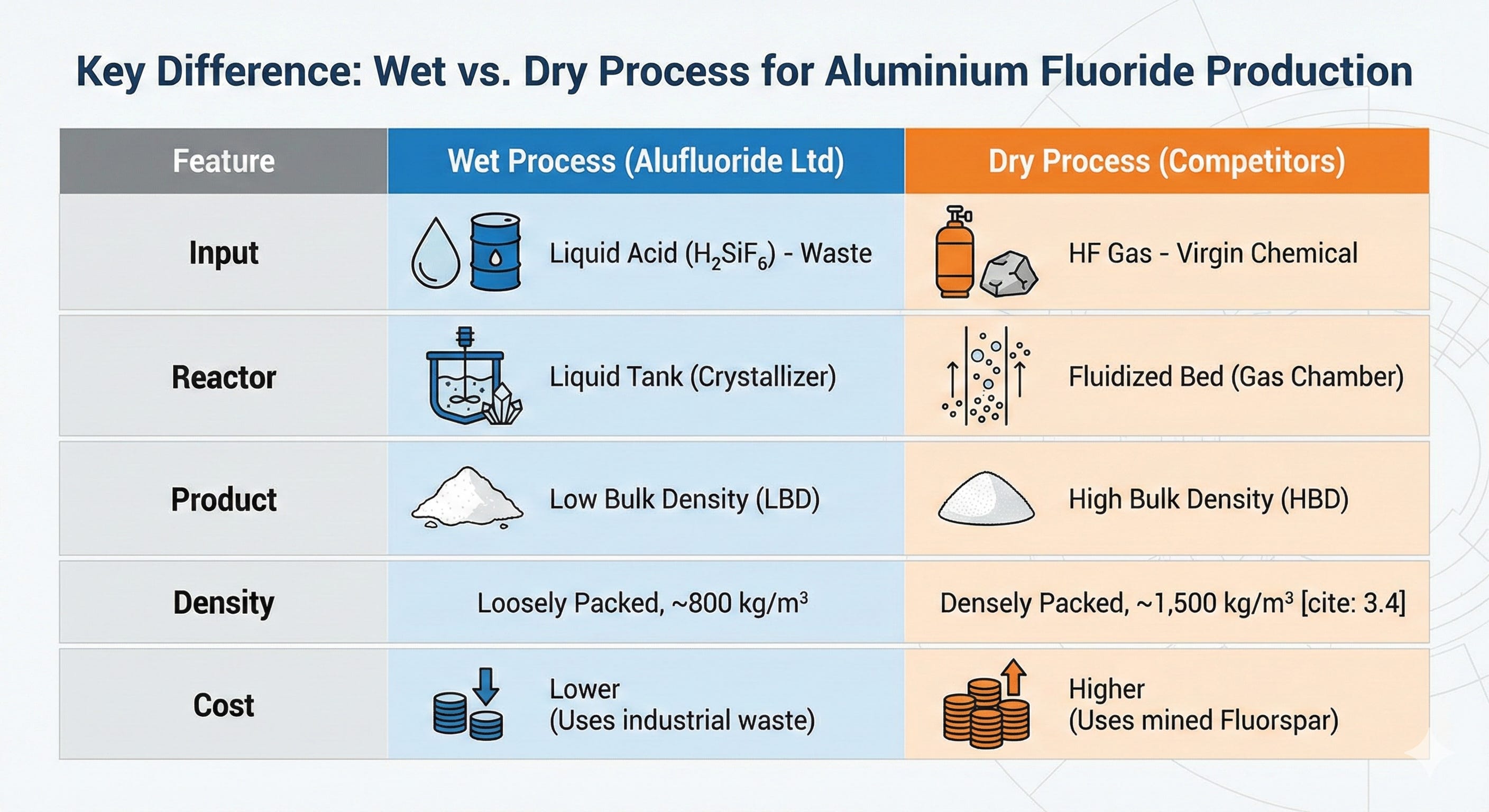

There are two methods to produce ALF:

Dry Process

Wet Process

In addition to getting a handle on How ALF is made, I recommend reading Appendix -1 (bottom section) on “WHAT CHEMICAL PROPERTIES A SMELTER WANTS IN ALF”

WHY IS THIS IMPORTANT?

From what we know at this point, Alufluoride does not run an imminent risk of “substitution” or an “obsolescence” risk, however, LBD & HBD ALF compete with each other.

Since our company is an LBD ALF player, we gotta know what its up against.

There are two methods of producing Alufluoride.

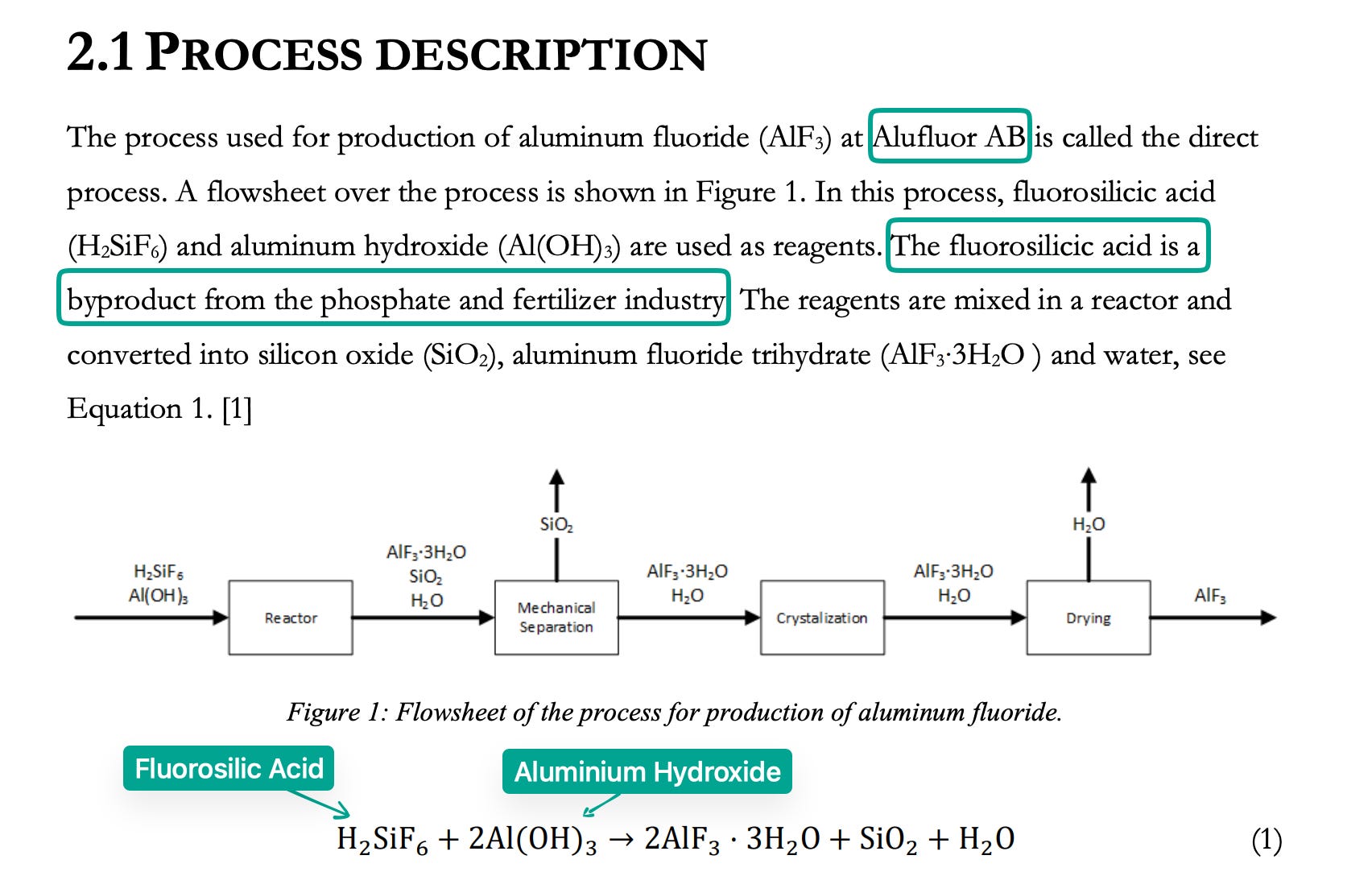

2.1 - Method 1 - The “Wet” Process.

Only ~20% of the World’s ALF production happens through this route.

Alufluoride Ltd uses this method, originally in technical tie-up with Alsuisse Ltd (a Swiss co’) which had patented a method for converting FSA (Fluorosilic Acid - waste from Phosphatic fertiliser Industry) into aluminium fluoride (AIF3) in 1973.

In 2000, Alsuisse Ltd was acquired by Alcan, a canadian Aluminium producer. It possible that this acquisition hampered continued technology partnership with our company.

Without getting into technicalities, this method produces Low Bulk Density Alufluoride or LBD ALF.

Because raw material (FSA - Fluorosilicic acid) is a waste byproduct of the Phosphatic fertiliser industry, this method enjoys a cost advantage over the “Dry Process”.

Alufluoride Ltd (18,000 TPA) & Greenstar (5000 TPA) are the two LBD ALF producers in India using the “Wet” Process.

However, FSA supply has been a REAL CHALLENGE for the company.

Infact, Alufluoride’s unit is built next to Coromandel International Ltd in Vizag because it had contracted 3000 TPA of FSA (Acid) from Coromandel at inception in 1995.

However, since Day 1 - FSA supply from the adjoining Coromandel unit has has been unreliable & patchy.

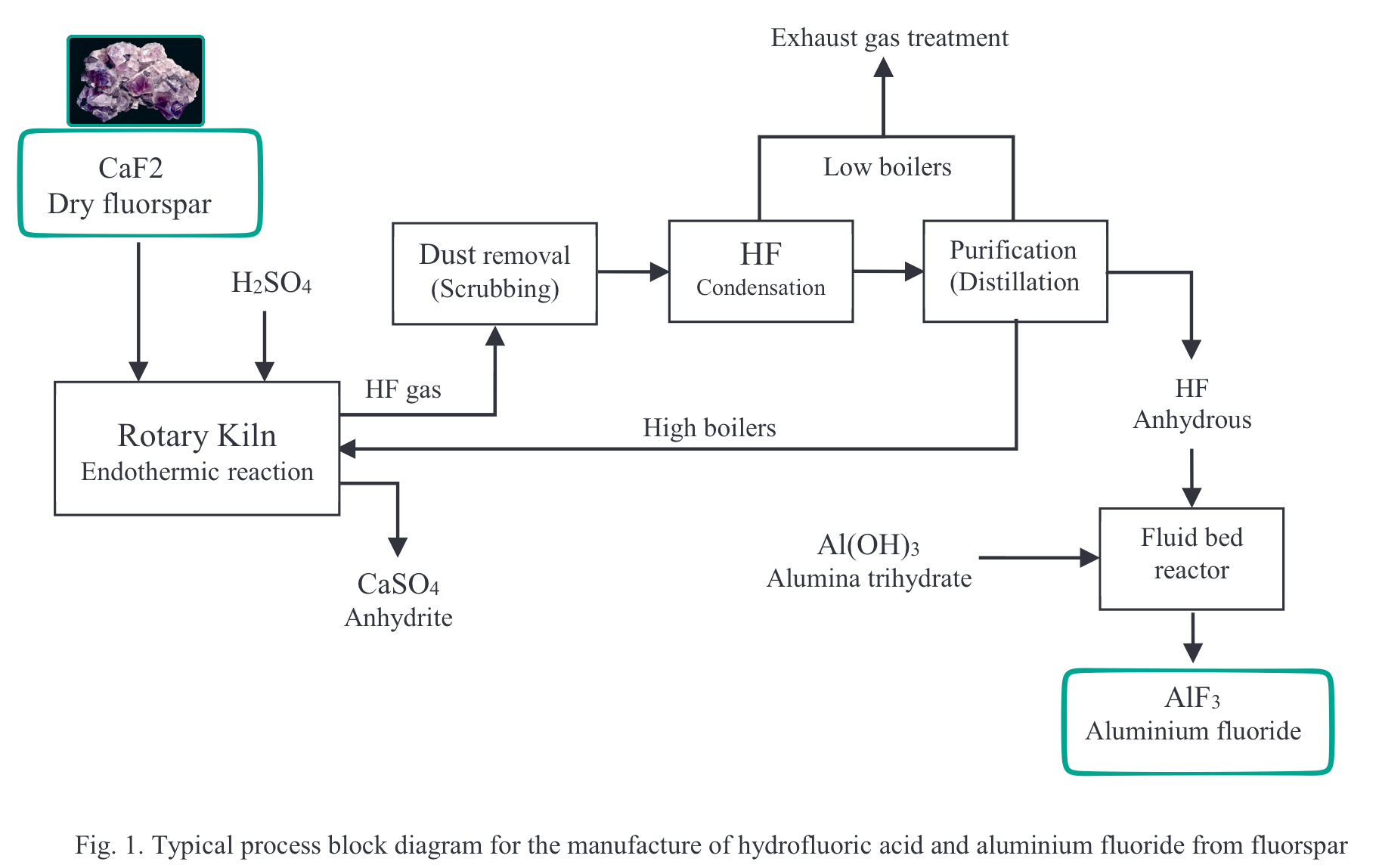

2.2 - Method 2 - The “Dry” Process.

This method requires mining fluorspar. It accounts for ~80% of the Global ALF production.

Typically, this method produces High Bulk Density ALF or HBD ALF.

China is the dominant force in global fluorspar mining. It accounts for ~6.0 MT production vs Global production of ~9.5 MT (2024), representing 63% of Global production.

3. Why this matters for our thesis?

This concentration is a major risk for competitors using the ‘Dry Process’ and a potential advantage for Alufluoride Ltd.

Supply Risk: With over 60% of supply coming from one country, any geopolitical tension or export restriction from China immediately spikes the price of Fluorspar.

Internal Consumption: China is no longer just exporting; it is consuming more of its own fluorspar for its massive EV battery industry (LiPF6 electrolyte). This means less fluorspar is available for the rest of the world, keeping prices high for global smelters.

Alufluoride’s Immunity: Since Alufluoride uses fertilizer waste (FSA) and not mined fluorspar, it is completely immune to this Chinese supply squeeze should it happen.

However, LBD ALF has its own disadvantages. More on that later.

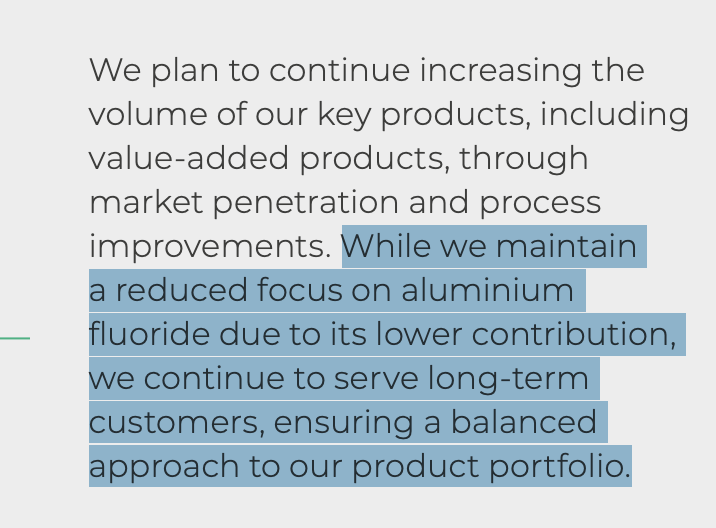

4. Major Alufluoride Competitor reducing focus on ALF

Tanfac Industries Ltd is a major ALF (Dry Process) player in India with Capacities of 16,500 TPA.

In its FY25 Annual Report, Tanfac Ind mentioned that as a means of reducing supply risks (Fluorspar import from China), it is “Broadening our supplier base to regions beyond China, securing alternative sources to reduce dependency & cost”.

So, Fluorspar imports expose companies taking the ‘Dry process’ route to supply risks.

secondly, If you’re going to use fluorspar you might as well get the “most out of it”.

Tanfac has consistently build capacities in downstream fluorine derivatives. That’s why it is strategically reducing focus on ALF with higher focus towards “downstream value added products like refrigerant gas”…

Through much of its 50 year history, Alufluoride Ltd has been a sleepy co’.

It has NOT “de-worsified” (hooray) nor has it built new or adjacent capabilities. This is possibly why Tanfac is a INR 3000 cr company today while Alufluoride is a INR 300 company despite both commencing production around 1994-95.

Anyway, the point we’re trying to make is that ‘Dry process’ has it own sets of challenges despite accounting for a major chunk of total Alufluoride sales worldwide.

“Dry process” looks something like this.

5. ALF Market Size in India

The market for ALF in India is about 70,000 to 80,000 TPA (Alufluoride Ltd management estimates quoted in AGM 2025).

Domestic capacities Include Tanfac (Dry - 16,500 TPA), Alufluoride (Wet - 18,000 TPA) & Greenstar (Wet - 5000 TPA). The balance ~50% is imported.

ALF demand is directly linked to : *Domestic Aluminium Smelting capacities.

*It does not export meaningfully as of FY25 but has done so in the past.

Current expansion plans indicate that by FY30, we’re looking at an incremental capacity of ~1.9 MTPA, that equals 38,000 TPA* of incremental ALF demand over the next ~4 years.

*(ALF required is ~2% of Aluminium by weight)

6. Alufluoride Ltd - Volume growth

Lens #1

The "hypothetical” runway for Alufluoride Ltd is longer because:

A. “Wet Process” Costs AND Prices are LOWER.

B. There is plenty of room for domestic players to expand & GROW FASTER THAN MARKET given ~50% of ALF is STILL imported.

This would mean Alufluoride SHOULD BE LOOKING TO EXPAND CAPACITIES AGGRESSIVELY. The challenge here is getting adequate FSA (Acid) supply.

Lens #2

All said and done, fact is ~70-80% of the World Aluminium alfuoride demand for smelting metal is met by HBD ALF.

Assuming the ratio of 80:20 - HBD to LBD remains constant by FY30 too, on an incremental demand of ~38,000 TPA, with LBD (Wet Process) ALF accounting for just ~20% of it = ~7,200 TPA.

EVEN IF Alufluoride Ltd (our company) manages to ADD the entire 7200 TPA.

Total Capacity = 18,000 TPA + 7200 TPA = 25,200 TPA.

That’s 12% CAGR man !! Hardly anything to go bonkers about.

However, 12% volume growth could potentially translate into higher EBITDA & PAT growth if margins expand.

6.1 - Can margins expand?

Margin expansion is a function of :

Utilisation levels

Increase in realisation/MT without corresponding increase in RM cost.

Reduce Conversion costs

Assuming utilisation levels are constant (they’re not), Its my humble submission that Increase in realisations/MT are outside the company’s control.

This leaves cost reduction as the ultimate lever of margin expansion.

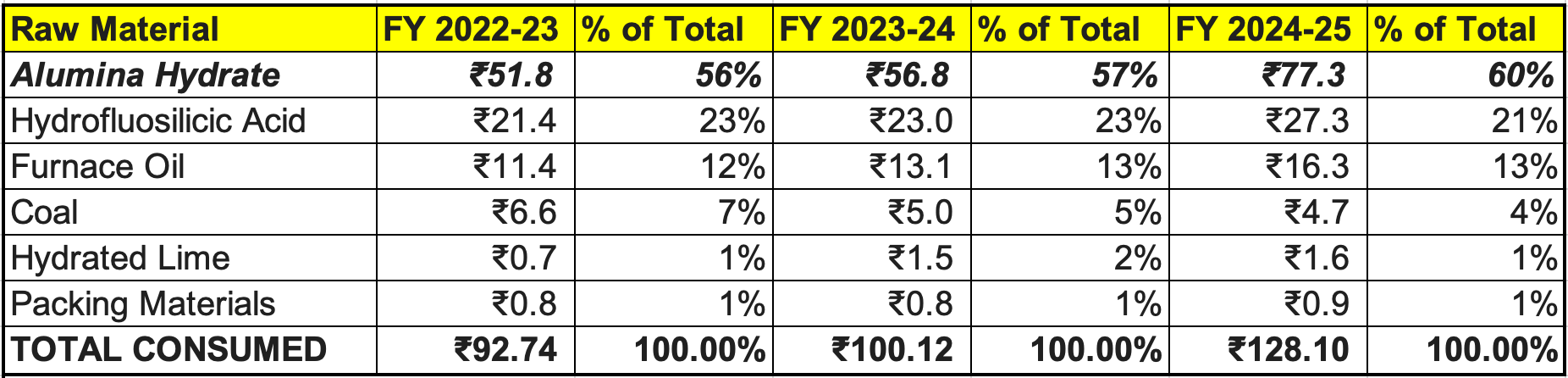

So, which costs to focus on? Here’s a breakdown of Raw Material costs.

Assumed you’re on the Board of Alufluoride Ltd, knowing what you know now, what costs would you reduce?

Since FSA supply is CRITICAL but outside company’s control AND/OR unviable to do in-house, the largest and single most impactful cost item is Alumina hydrate ( Alumina with water), which contributes consistently over 50% to the overall cost.

As a capital allocator (Management) I would be urged to manufacture Alumina Hydrate in-house, if it made economic/operational sense.

Does it?

Here are some estimates/moves in this direction:

On 10th March 2025 – Board approved alteration of objects clause in MoA to include “manufacture, importer and export, trading and sale of Alumina Hydrate or other associate minerals.”

Subsequently, Shareholder Approval was initiated on 20th April 2025 via postal ballot - “the Company is exploring a new project to manufacture Alumina Hydrate. To initiate this project the objects of the Company were to be amended...” (FY25 Directors’ Report).

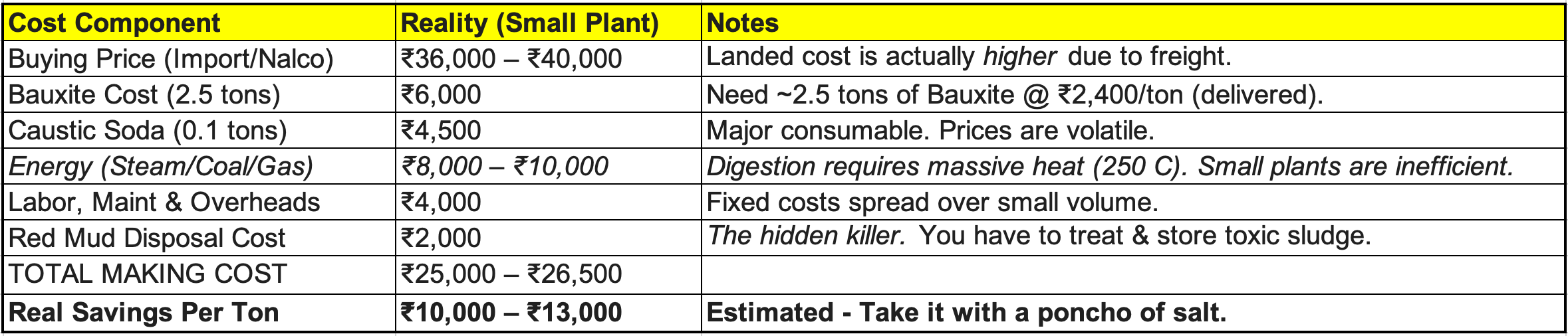

Cost saving per ton of Alumina Hydrate by virtue of this project are estimated at ~ INR 10,000/ton.

If this were accurate, the company would save 18,000 MT (Alumina hydrate) * INR 10,000/Ton - INR 13,000/Ton (cost saving) = INR 18 Cr - INR 23 Cr

Thumb rule: 1.03x Alumina Hydrate required for every 1 ton for Alufluoride produced.

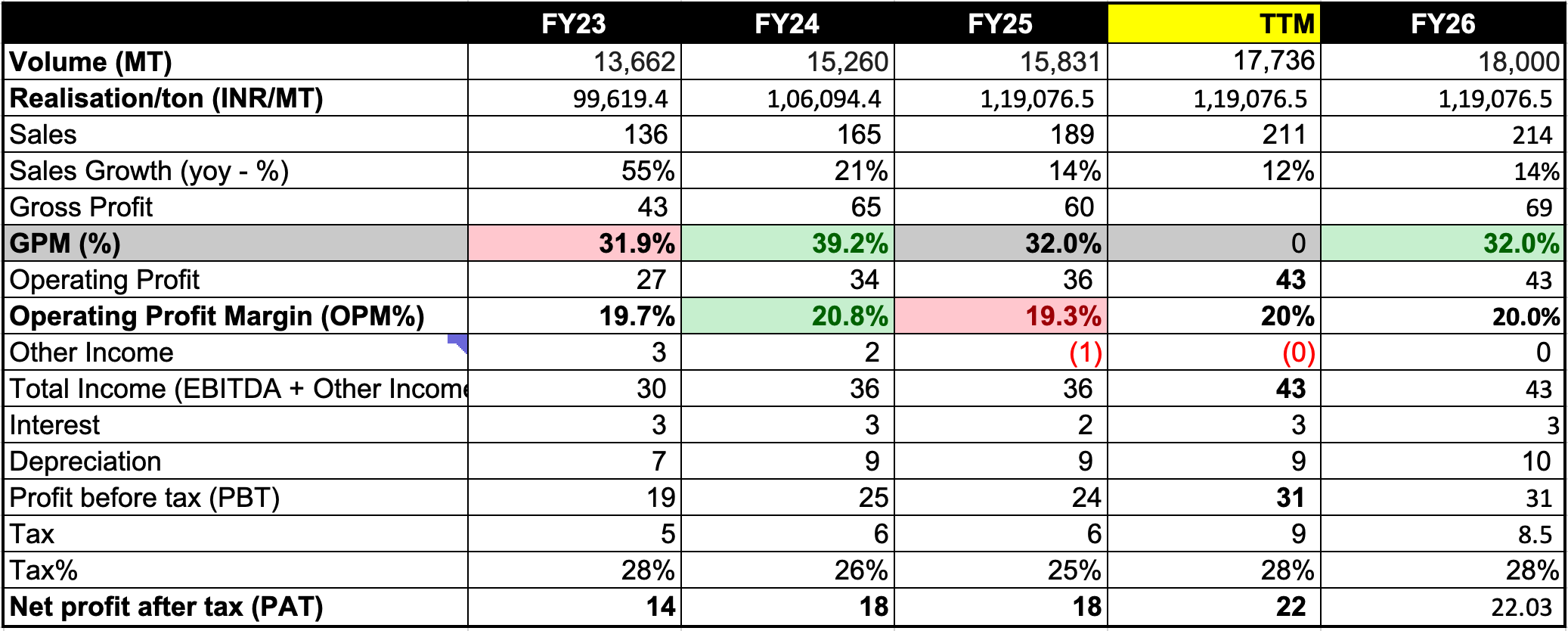

For context, the company reported INR 22 cr PAT in FY25.

In the AGM 2025 - Managing Director Venkat Akkineni provided “ballpark figures” for the investment:

Phase 1 Cost: ₹40 – ₹50 Crores

Capacity: To produce 50,000 Tons of Alumina Hydrate.

Internal Requirement: The company anticipates its own future requirement to be ~30,000 Tons. The surplus (~20,000 Tons) will likely be sold to third parties.

Phase 2 Cost (Optional): ~₹30 Crores

Capacity: Expansion by another 40,000 – 50,000 Tons.

Total Potential Investment: ₹70 – ₹80 Crores (if both phases are executed).

This means IF (big if) & when this project is successfully commissioned, even IF sales & profitability remained at similar levels, it would theoretically double the bottom line.

(Actually there would be higher depreciation & Interest costs but you catch the drift, right? - The project makes a lot of sense)

Realistically, its early days for this project. The Board has recommended a Techno-feasibility study and given the change in MOA, the company appears serious, not to mention it makes a LOT of financial & strategic sense. \

Other than the backward integration of Alumina Hydrate, the co’ is reducing power/electricity costs too.

It is investing in Solar Energy. Solar Power Plant of 1.1 MW shows under Capital Work-in-Progress (CWIP) at ₹409.86 lakhs, with completion expected in less than 1 year (Note 5.02 - FY25 Annual Report).

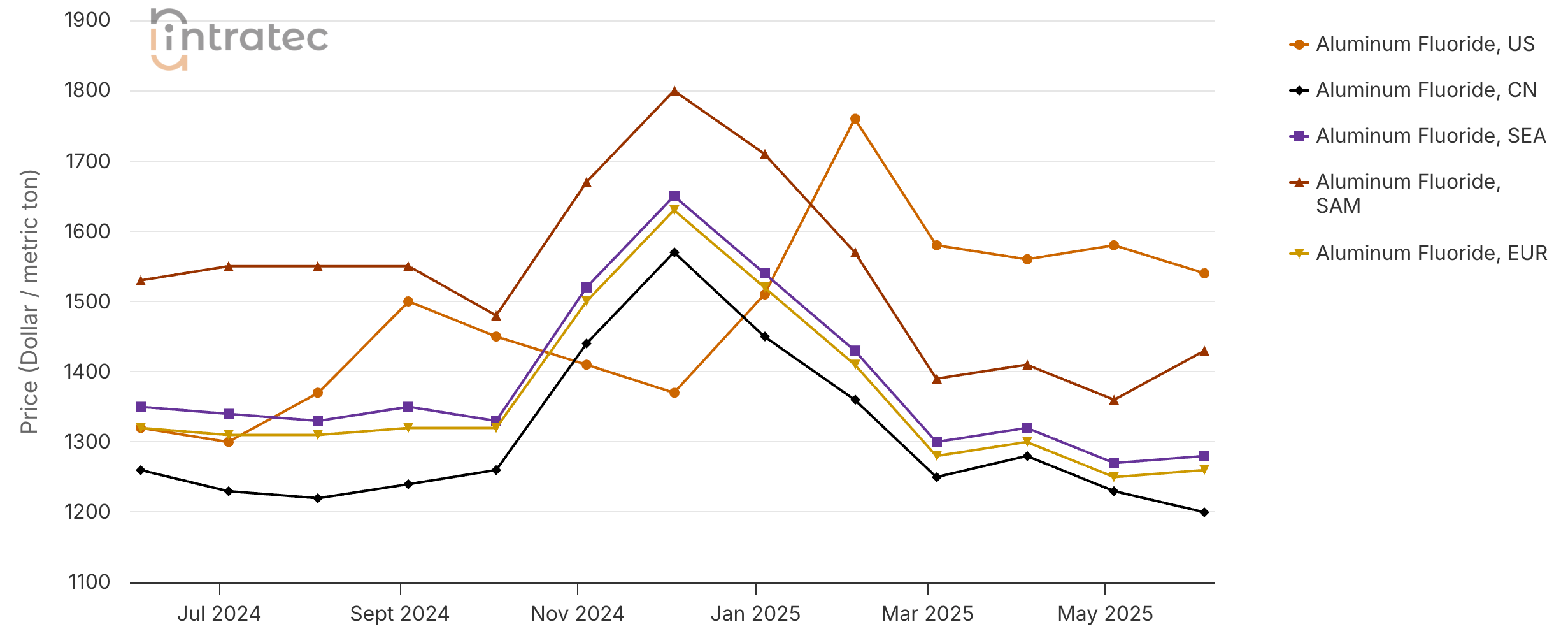

7. Alufluoride Ltd - Price growth.

I do not have a view on prices. They should range between $1200 - $1300/ton. The more the merrier.

8. Financial Analysis

Capital efficiency :

The co’ consistently earns a high return on capital employed. Note, Current Work in Progress numbers are not taken into consideration for the purpose of this calculation.

Growth :

The co’ capacity increased to 18,000 MT in May 2025 (from ~15,000 MT). The ramp-up seems to be going on point and TTM PAT is up nearly 22% up from FY25.

My estimate is that for FY26, at 18000 MT volume & last year reliasation/ton we’re not going to see major upside from what we’ve already seen in TTM numbers.

However, at 14.5X P/E multiple, this growth seems to have been ignored by the market.

There are no other reported plans on the horizon for volume expansion - which requires contracting additional quantities of FSA - a challenge which the co’ has repeatedly lamented about in every annual report.

However, I expect the co’ to announce a capacity expansion within the next financial year.

Even if capacity expansion is not announced and meanwhile - the alumina hydrate - backward integration plans materialise & are executed, operationalised & commissioned fully within 3 years from now (FY29), we could see significant jump in PAT on the back of this project. Check estimated numbers above.

Debt position

The Balance sheet looks clean with minimal debt. The company is net cash company.

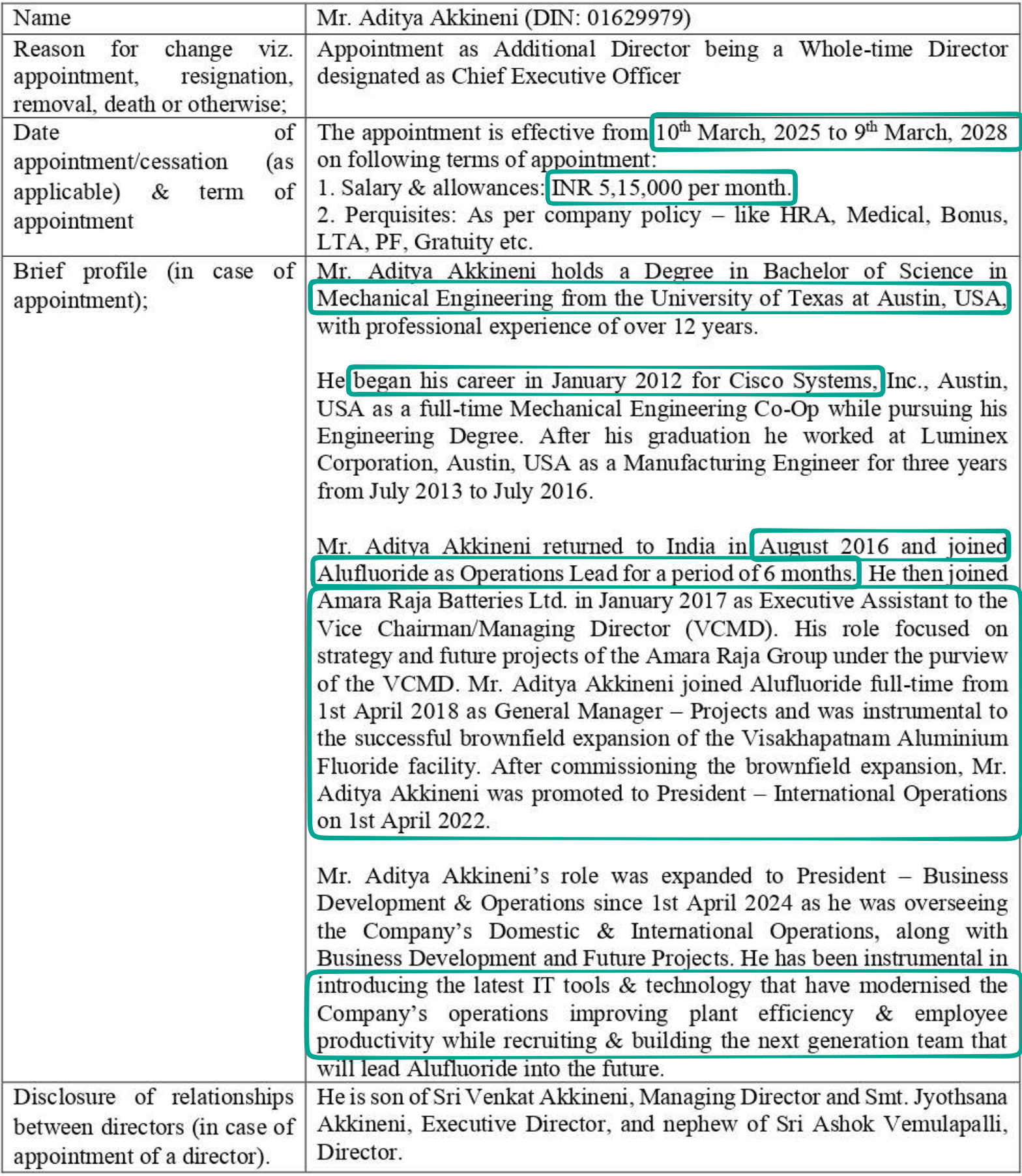

9. Managment

The thesis hinges on Aditya Akkineni, who after about 8 years of joining operations has been elevated to the post of CEO on 10th March 2025.

Other than the relatively rapid increase in capacity since 2017 (co-incides with him joining the co’), Aditya brings in an interesting skill set and more than anything fresh energy.

How the new CEO manages to expand & execute new projects such as Alumina Hydrate will be interesting to watch. Since the company has historically been really poor at communicating with shareholders we’re hoping this changes with the new CEO taking charge.

10. The Thesis

The Indian Aluminium Industry is in expansion mode. Proxy players like Alufluoride Ltd have a clear runway for growth if they can solve for RM supply issues (Wet process) and have the hunger to grow. The new CEO exhibits those characteristics.

Recent PAT growth of 22% has been ignored by the market. The co’ trades at 14.5X PE. The EV/EBITDA is 8X. Nice BUT NOT obscenely undervalued.

The co’ is a Net Cash co.

The business is a high ROCE business and can fund growth internally.

The backward integration of Alumina hydrate + 12% volume growth are two key triggers for growth.

The co’ has minimal RPTs and/or corporate governance concerns.

11. The Anti-thesis

Stories are good. Execution is better. The above projects need to be executed for numbers to show.

69% of sales is to one customer. This is the case with all suppliers to aluminium smelters because there are only 3 in India. While long term I don’t have a reason to believe this could be a problem - in any given year or two the co’ could potentially lose a big chunk of its sales.

That’s it folks.

Please remember to Do your own research. This should serve as a lead NOT a recommendation.

In case you smell bullshit and/or have a differentiated insights and/or a question or opinion please do let me know in the comments.

Yours sincerely

Rahul Rao, CFA

Note: We have relied on data from www.Screener.in and www.tijorifinance.com throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educational purposes only.

Rahul Rao has been Investing since 2014. He has helped conduct financial literacy programs for over 1,50,000 investors. He helped start a family office for a 50-year-old conglomerate and worked at an AIF, focusing on small and mid-cap opportunities. He evaluates stocks using an evidence-based, first-principles approach as opposed to comforting narratives.

Disclosure: The writer or his dependents Hold shares in the securities/stocks/bonds discussed in the article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.

Appendix -1

WHAT CHEMICAL PROPERTIES A SMELTER WANTS IN ALF

Here they are:

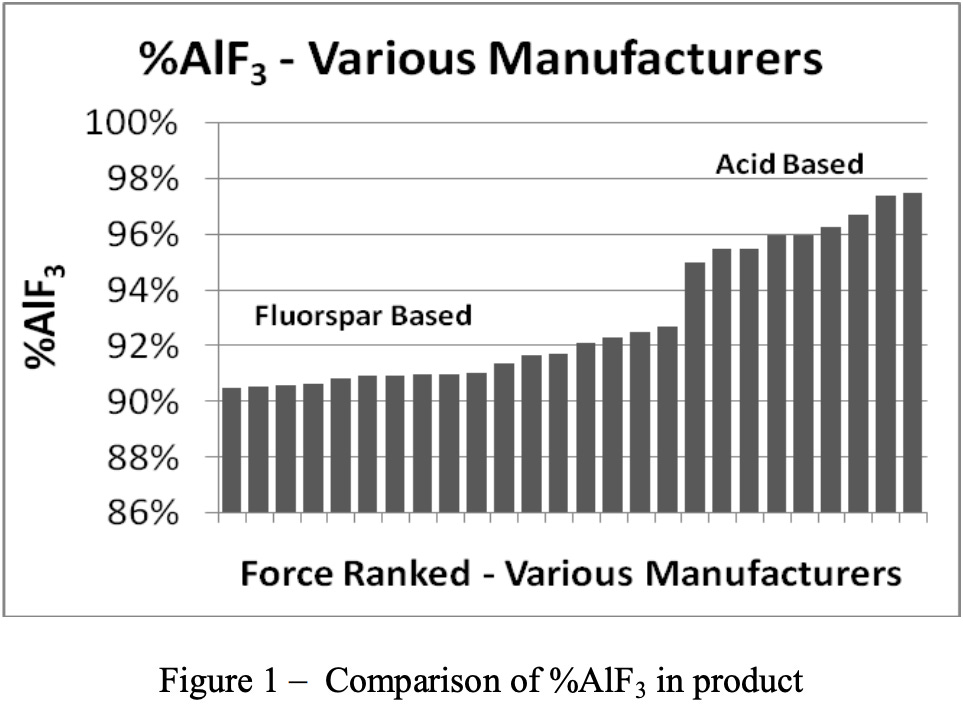

High ALF3 purity (% terms): Between the two method - Acid based (Wet process) provider a higher ALF%.

Batch to Batch variation in Quality needs to be low: Smelters need to watch out for too much variation in ALF% from batch to batch.

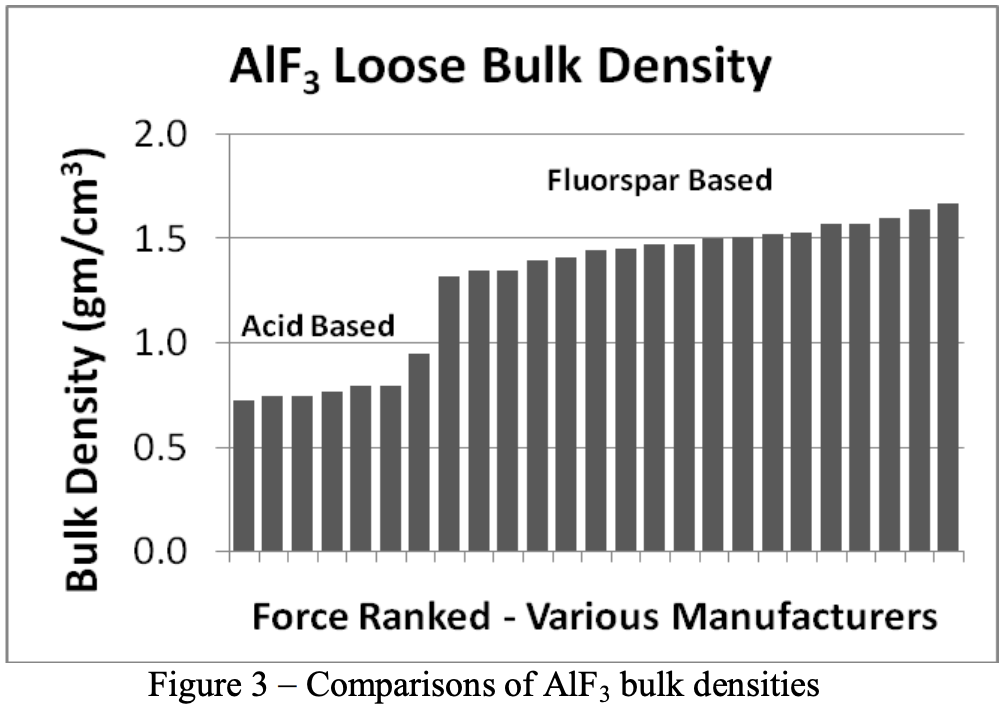

Bulk density : ALF is used in two places in the smelting process - Reduction cells (1) and crucibles (2)

Additions of AlF3 to reduction cells (1) and crucibles (2) are often made on a volumetric basis. This means that differences in bulk density will need to be taken into account for distribution and dispensing of AlF3.

This is Nerdspeak for - HBD - High Bulk Density ALF (Dry Method) is mostly preferred in Reduction cells (1) & LBD - Low Bulk Density ALF is better suited for Crucibles (2).

Reduction cells is the “pot”. Crucibles comes in the next step - its a “separate bucket” used to pour out the actual metal.

Low impurities such as Phosphorous & Silica.

NOTE: Please note the above conclusions are taken from a 2010 Paper comparing two methods of Alufluoride production - Wet vs Dry Process & a samples from suppliers of LBD & HBD ALF.

AGM :

Leading companies in Alufl: https://www.linkedin.com/pulse/leading-companies-aluminum-fluoride-alf-strategic-insights-desai-oyq7f/

Alufluor - World Leader in Wet Process : https://www.alufluor.com/company/our-history/

Buss Chemtech now has the Technology for Wet method: https://www.buss-ct.com/fluorine-chemistry/low-bulk-density-aluminum-fluoride/

Alu fluoride prices : https://www.intratec.us/solutions/primary-commodity-prices/commodity/aluminum-fluoride-prices