Inox Wind Valuation Update [Q4 FY24]

Inox Wind Valuation Update [Q4 FY24]

Slower than Expected Execution.

🌟 Q4 Results not as per expectations

🌟 Deliveries (MW) & Interest Expenses will be Key Monitorables going forward

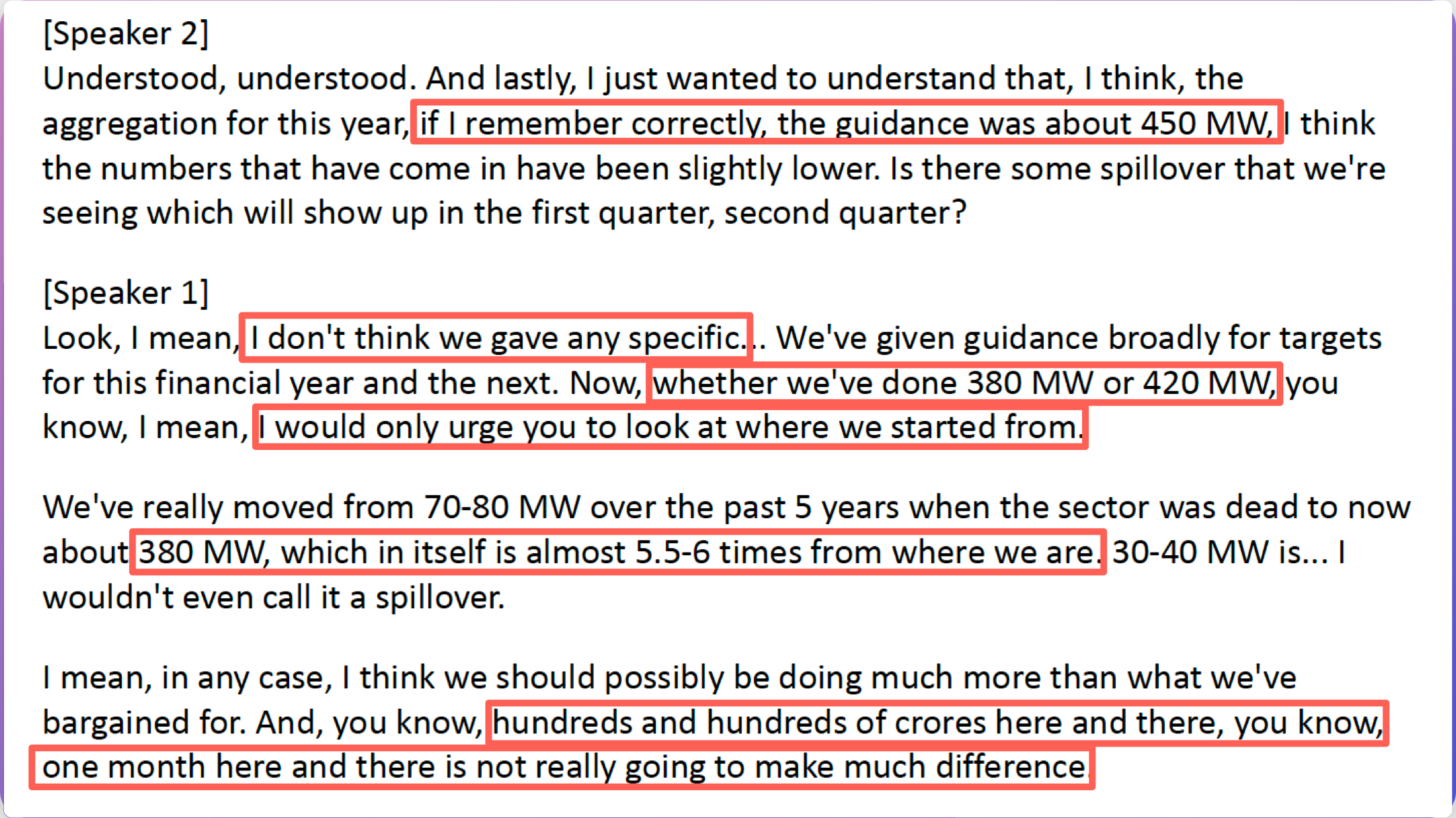

Inox Wind Ltd was expected to deliver (or Execute) ~500 MW of Wind Energy Equipment in FY24.

Although on a yearly basis, the execution was ~3.5X compared to last year, Markets are forward-looking and Expectations of 500 MW had been ‘priced in’. The Actual execution was close to ~25% lower than ‘Expectations’.

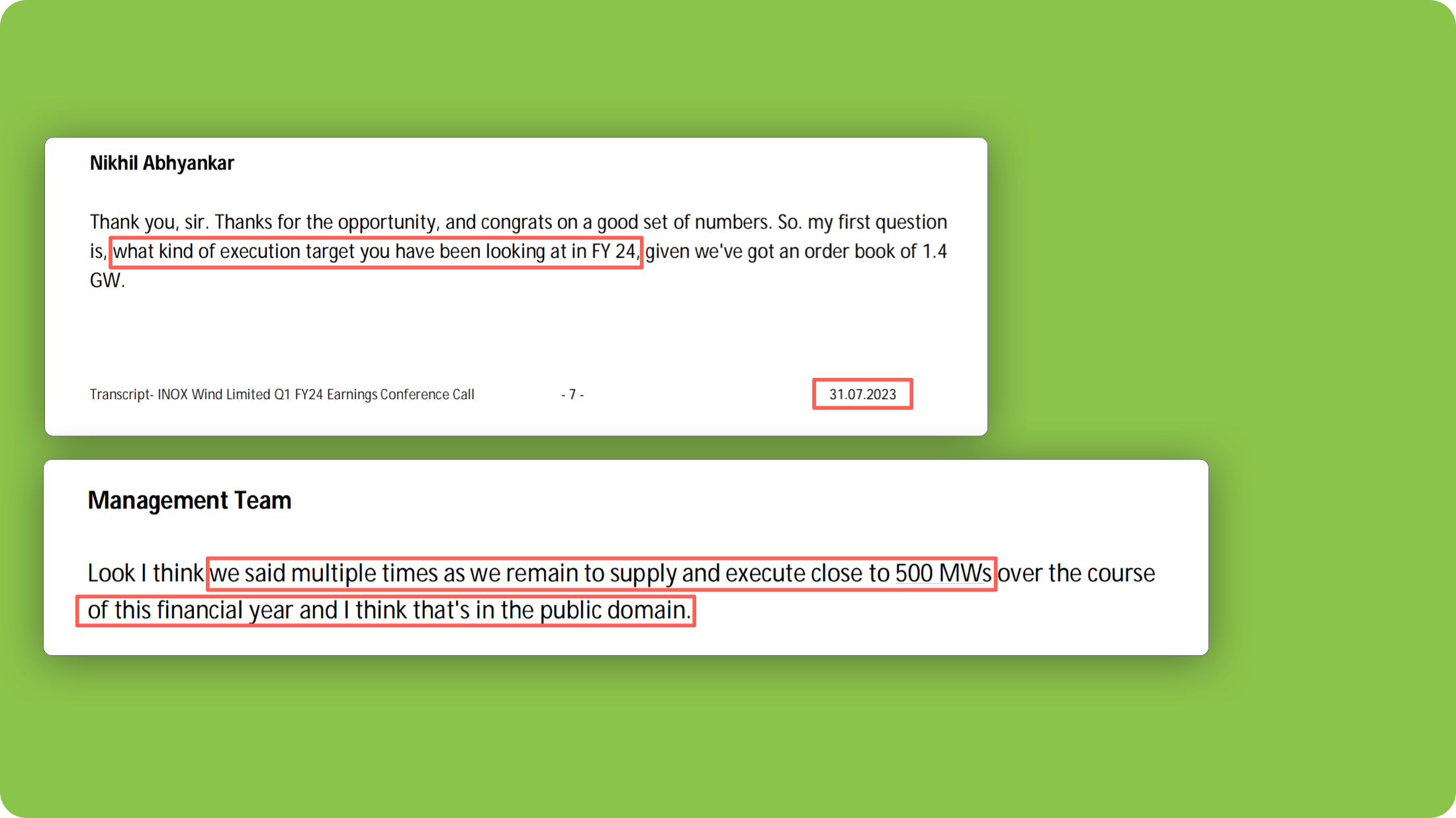

At the end of Q2FY24, when asked whether 500 MW would be on track, Management said we’re ramping up and that “every Quarter should be better than the last” and so it has been except…

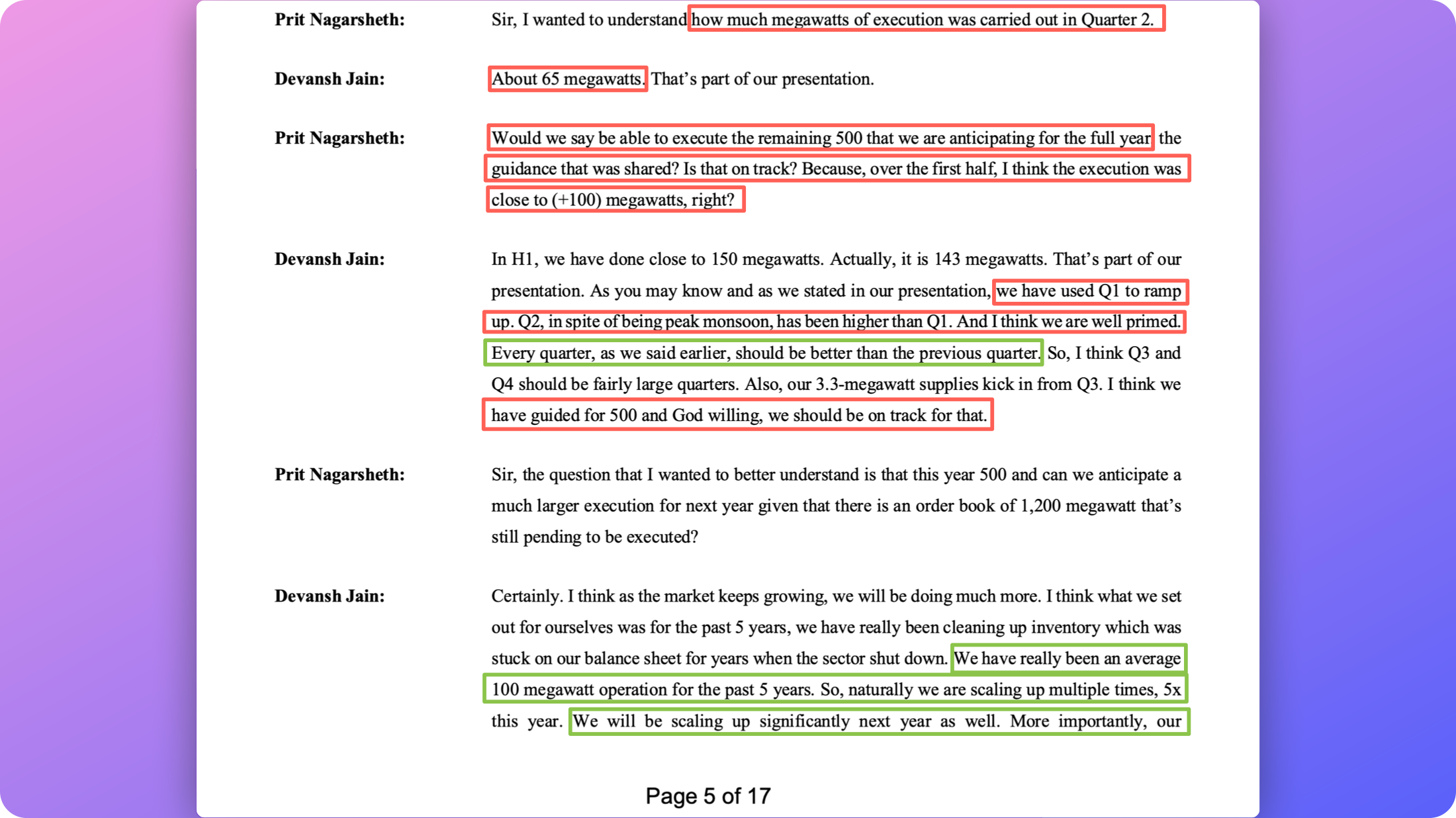

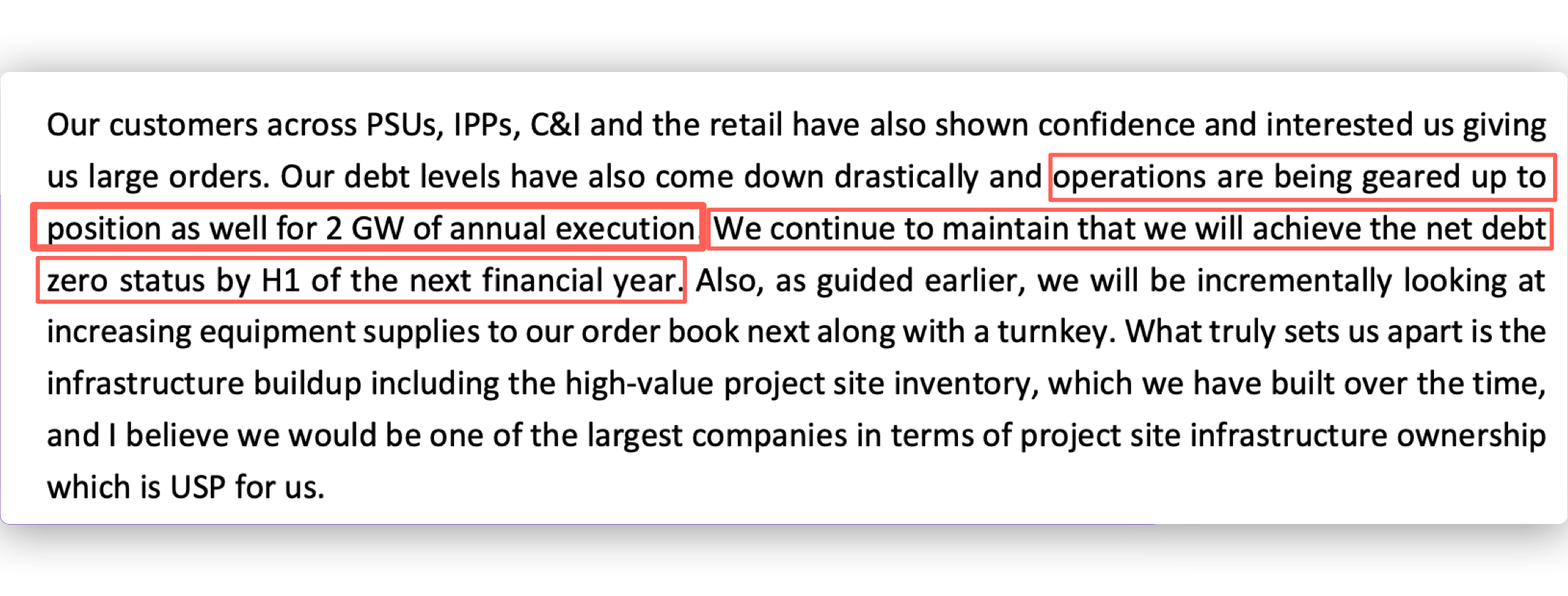

By the end of the December 2023 Quarter, Managements outlook and commentary remained bullish (104 MW Execution in Q3) and references were made to “2W Annual execution” (Think big, they say)

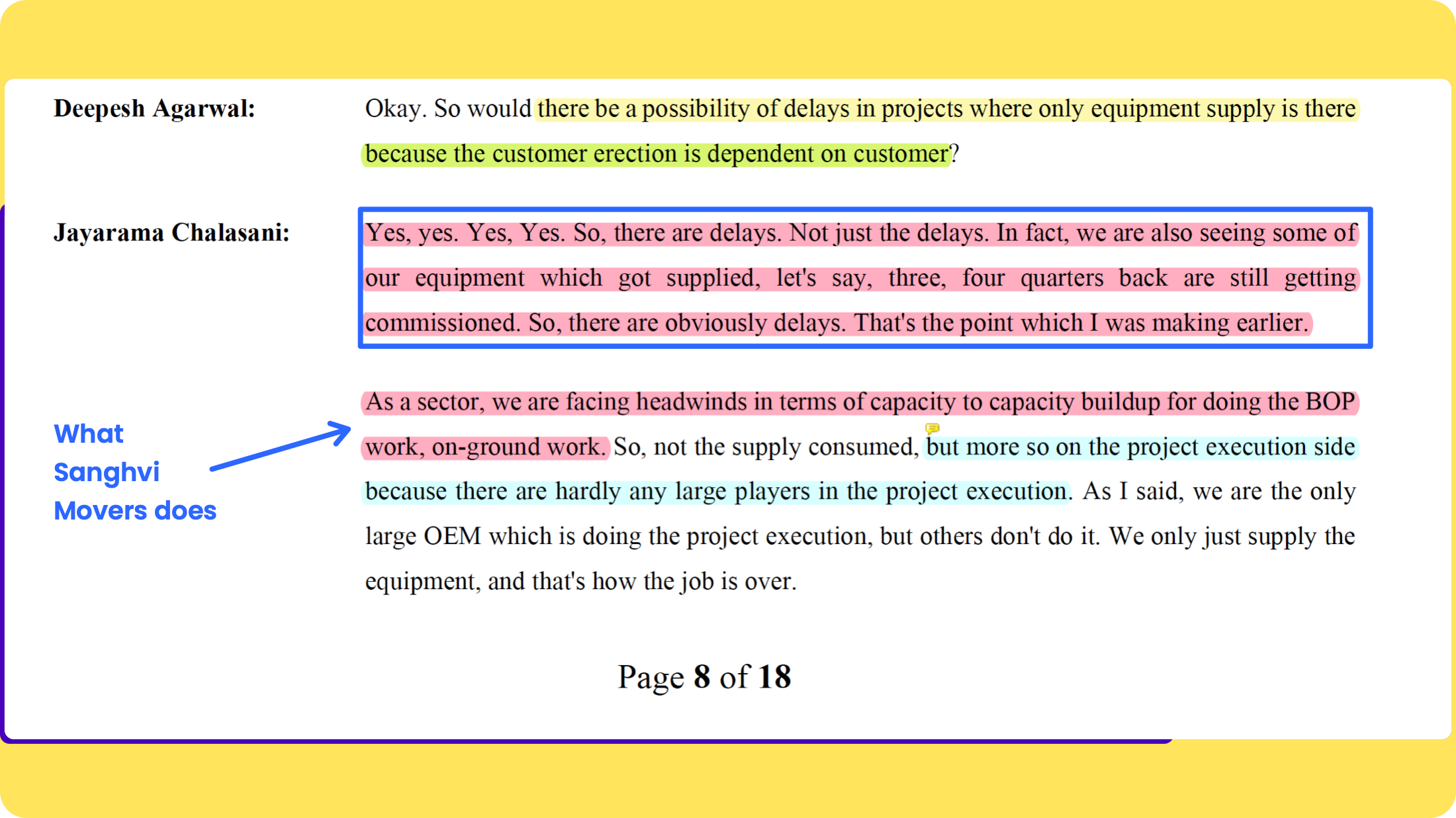

Meanwhile, Suzlon was reporting scarcity of EPC guys (think : Sanghvi Cranes) and slow execution on account of the Evacuation Grid not being ready.

“It appears that its Customers (IPP - Independent Power Producers) are running into execution problems - Land Acquisitions, Grid Connectivity, and a shortage of EPC guys (such as Sanghvi Movers)” Suzlon Valuation Update

When Inox Wind Management was asked to verify if this was the case on the ground, they used this opportunity to highlight the merits of their own Order book - EPC + Equipment Delivery whilst simultaneously sh*t*ing on Suzlon’s Equipment only focus.

They alluded to the fact that while Suzlon may have EPC issues they (IWL) do NOT because of their ‘plug & play’ Infrastructure and ‘EPC capabilities’

All that Rah-rah and It turned out that by the end of Q4, Inox Wind has fallen well short of their 500 MW target/expectation.

All said and done, despite my mocking tone I remain cautiously optimistic of the co’ prospects given their relatively favorable (NOT CHEAP) valuations and prospects.

Bottomline is :

Q4 Results were NOT Great from the vantage point of ‘Expectations’ that had been set. From the vantage point of FY23 executions, 3.5X Executions in FY24 obviously are spectacular but all that is already ‘priced in’

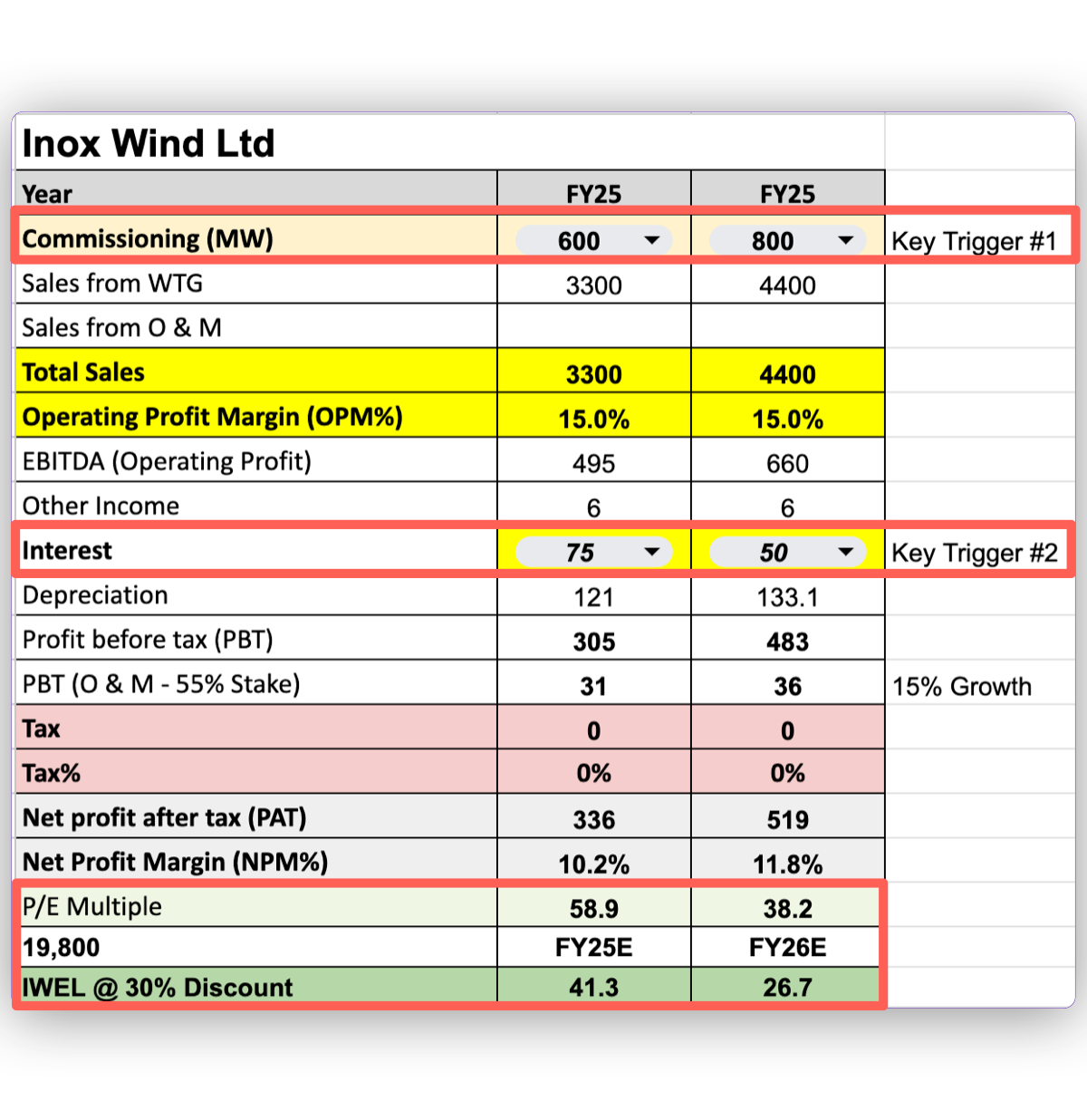

IWL Management has not upped the FY25 Execution to 800 MW !! I remain skeptical until proven otherwise [Will watch Q by Q developments closely]

The Biggest Trigger for boosting Earnings is reducing Interest expense. Every Single Cr saved goes straight to the bottom line ! The co’ is expected to be ‘Net Debt Free’ which means Debt - Cash = 0. Debt mainly in the form of working capital will remain.

In the last valuation note, my estimate (subjective and open to errors) was that IWL (standalone) was trading at a ~ 37X, 1 Year Forward multiple assuming you acquired shareholding via IWEL (Merger Arbitrage)

TODAY, at a higher Market cap (19,800 Cr) my estimates are that NOW, IWL trades at a higher 1-year forward multiple of 45X (41X on a Inox Green Consol basis) if acquired via IWEL (Merger Arbitrage)

Look forward to hearing your thoughts in the comments

Rahul

Disclaimer

Nothing you read here should be construed as investment advice. I do not know your circumstance so please treat the above as nothing more than my personal opinion, which is subject to change without prior notice to you. Please do your work and consult your financial advisor. I may own positions in all stocks, sectors and indices discussed and can exit them without notice.